Why Choose Us?

0% AI Guarantee

Human-written only.

24/7 Support

Anytime, anywhere.

Plagiarism Free

100% Original.

Expert Tutors

Masters & PhDs.

100% Confidential

Your privacy matters.

On-Time Delivery

Never miss a deadline.

1

1.Business management identifies that the longer an accounts receivable remains outstanding, the less likely the business will collect the receivable from the customer. Identify a method/approach that is appropriate for accounting for uncollectible receivables in this case and describe the method/approach including why it is appropriate (when describing, please describe how bad debt expenses are recorded using the method/approach, and/or provide an example of the journal entry required). Identify and describe the method/approaches that are less appropriate for accounting for uncollectible receivables in this case (when describing, please describe how bad debt expenses are recorded using the method/approaches, and/or provide examples of the journal entries required). (8 marks)

Clearly label each part of your answer as follows:

Appropriate method and approach is..........

Less appropriate methods and approaches are.........

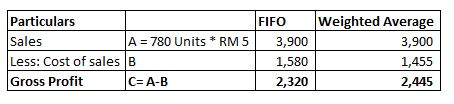

2.The following information is taken from the records of WeBs Sdn Bhd. The company uses the perpetual inventory system. Date Description Units Unit Cost (RM) Dect Opening inventory 100 1 Dec 5 Sale 80 Dec 6 Purchase 200 Dec 12 Purchase 125 2. 3 Dec 13 Sale 300 Purchase 350 2 Dec 19 Dec 29 Dec 30 Purchase 150 1 Sale 400 Required: (a) Calculate cost of goods sold and the cost of ending inventory under each of the following inventory cost flow assumptions: (0) FIFO (m) Weighted average [11 mark] BBM 205/03 (b) Assume each unit was sold for RM5. Complete the following partial income statements : (4 marks] FIFO Weightage Average Sales Less: Cost of Sales Gross Profit

Expert Solution

1.A bad debt expense is recognized when a receivable is no longer collectible because a customer is unable to fulfill their obligation to pay an outstanding debt due to various reasons

The appropriate method is using accounts receivable is aging method and approach is grouping all accounts receivable by age and certian percentage is assigned to each group ( this percentage is calculated or derived from using statistical methods and past experience )

The sum total of all groups result are deemed uncollectable

Eg : If a company has $100000 accounts receivable less than 30 days outstanding and $50000 accounts receivable outstanding for more than 30 days, Based on statistical model or past experience, receivable outstanding for less than 30 days is estimated 1% uncollectable and receivable outstanding for more than 30 days is estimated 5% uncollectable then ;

100000 ×1% =1000

50000 × 5% = 2500

A sum of $3500 is created as provision bad debt expence

Journal entries

Credit Sale

Accounts Receivable (Debit)

Sale Account (Credit)

Creating Provision for Bad Debt

Allowance for doubtful accounts (Debit)

Account Receivable (Credit)

Bad Debt realization

Bad debt expence (debit)

Allowance for doubtfull accounts (credit)

The less appropriate method is Direct write off method and the process is to recognize uncollectable accounts and directly write off those accounts as bad debt expences this method is used for Us Tax purposes but this method goes against Matching principle of accrual accounting and GAAP

The matching principle requires the expences to be matched with related revenues in the same accounting period

Journal entry for Diarect Writeoff method

Bad debt expence (Debit)

Accounts receivable (Credi)

2.

(i) Computation of Wesb Sdn Bhd Cost of Goods sold & cost of ending inventory using FIFO:

Under the FIFO method, the earliest goods purchased are the first ones removed from the inventory account.

Ending inventory units = Opening Inventory + Total purchase units - Sale units

Therefore, Ending inventory units = 100 + (200 + 125 + 350 + 150) - (80 + 300 + 400)= 100 + 825 - 780 = 145 units

Hence, the ending inventory of 145 units will be 60 units from purchase on Dec 29.

Hence, Cost of ending inventory = 145 units * RM 1 = RM 145

Cost of goods sold under FIFO = Cost of opening Inventory + Cost of purchases - Cost of ending Inventory

Cost of opening goods = 100 units * RM 1 = RM 100

Cost of Purchases = (200 units * RM 2 + 125 units * RM 3 + 350 units * RM 2 + 150 units * RM 1) = RM 1,625

Cost of ending Inventory = RM 145

Hence, Cost of goods sold under FIFO = RM 100 + RM 1,625 - RM 145 = RM 1,580

(ii) Computation of Wesb Sdn Bhd Cost of Goods sold & cost of ending inventory using Weighted Average Method:

Under weighted average method,

Cost of Goods sold = Weighted average cost of purchase*No of units sold

Cost of ending inventory = Weighted average cost of purchase*Ending inventory units

Weighted average cost of purchase = (Cost of opening goods + Total cost of goods purchased)/(Opening Inventory + Total purchase units)

Weighted average cost of purchase = ( RM 100 + RM 1,625 ) / (100 + 825) = RM 1.6485 per unit

Cost of Goods sold using weighted average method = 780 units*RM 1.6485 = RM 1,455

Cost of the ending inventory using weighted average method = 145 units*RM 1.6485 = RM 270

(b) Partial Income Statement will be as follows:

please see the attached file.

{kind=link}

Archived Solution

You have full access to this solution. To save a copy with all formatting and attachments, use the button below.

For ready-to-submit work, please order a fresh solution below.