Why Choose Us?

0% AI Guarantee

Human-written only.

24/7 Support

Anytime, anywhere.

Plagiarism Free

100% Original.

Expert Tutors

Masters & PhDs.

100% Confidential

Your privacy matters.

On-Time Delivery

Never miss a deadline.

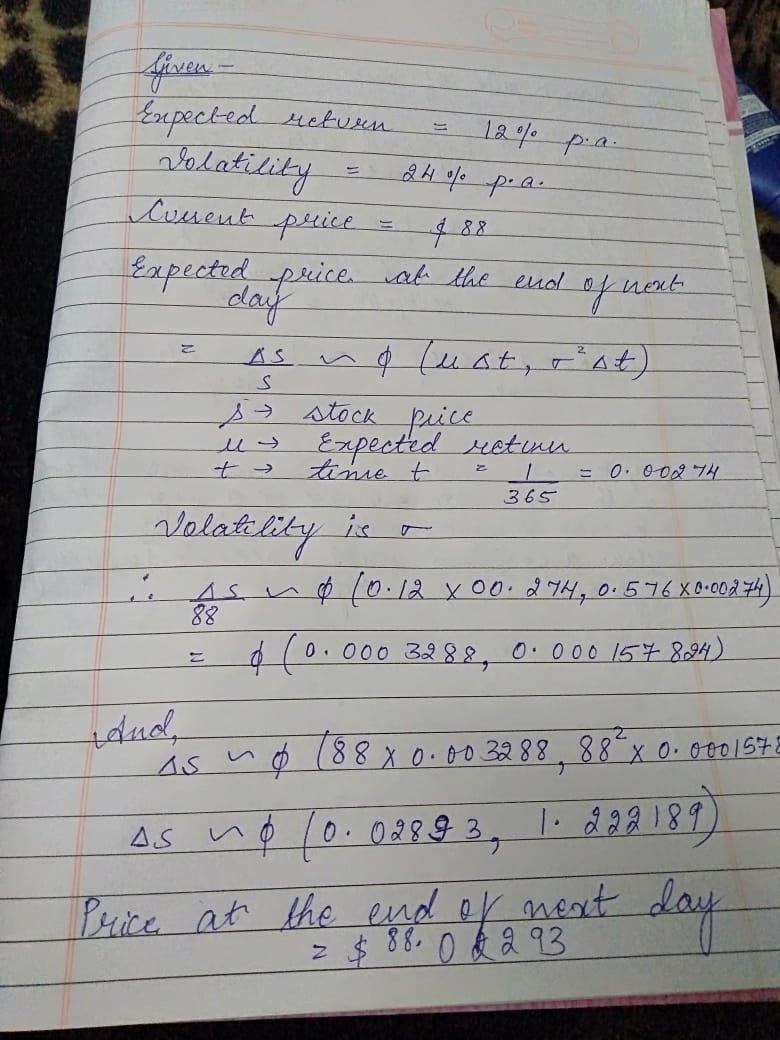

Suppose that the price (S) of a stock has an expected return of 12% per annum and a volatility of 24% per annum

Suppose that the price (S) of a stock has an expected return of 12% per annum and a volatility of 24% per annum. The stock price is currently $88. (a) Calculate the expected stock price at the end of the next day. (b) Calculate the standard deviation of the stock price at the end of the next day. C) Find the 95% confidence limits for the stock price at the end of the next day. (d) If you are to do the same for the stock price at the end of the month, assuming that it is the beginning of a month now, is it appropriate to use the same method as above? Explain.

Expert Solution

Please see the attached file

{kind=link}

Archived Solution

You have full access to this solution. To save a copy with all formatting and attachments, use the button below.

For ready-to-submit work, please order a fresh solution below.