Why Choose Us?

0% AI Guarantee

Human-written only.

24/7 Support

Anytime, anywhere.

Plagiarism Free

100% Original.

Expert Tutors

Masters & PhDs.

100% Confidential

Your privacy matters.

On-Time Delivery

Never miss a deadline.

Sam has $10,000 and is considering investing in two stocks - HSCC and Ninecent

Sam has $10,000 and is considering investing in two stocks - HSCC and Ninecent. The followings are the returns of these stocks under different states of affair Probability 0.2 HSCC 2% Ninecent 16% State of Affair Pandemic No Pandemic (Normal) No Pandemic (Boom) 0.3 3% 10% 0.5 14% 5% a) Calculate the expected rate of return, variance and standard deviation of HSCC & Ninecent (6 marks) b) Suppose Sam forms a portfolio with the stocks of HSCC and Ninecent. If he wants the portfolio to have 8.6% expected return, how much should he invest in HSCC? Calculate the variance and standard deviation of this portfolio given the covariance between HSCC and Ninecent is -0.0022 (or -0.22%). (8 marks) c) Explain why the risk of Sam's portfolio is lower than the weighted average risk of HSCC and Ninecent (4 marks) d) Suppose the risk-free rate is 3%, the market risk premium is 6% and the betas for HSCC and Ninecent are 0.7 and 1.3 respectively. Using the CAPM model, estimate the required rates of return of HSCC & Ninecent. (6 marks) e) Should Sam buy HSCC or Ninecent? Justify your answer by checking whether the two stocks are overpriced or underpriced. (4 marks) 1) Ninecent is having higher beta while HSCC is having larger standard deviation. Explain why the results of beta and standard deviation can be different even though both of them are measuring risk.

Expert Solution

Massive calculations are required . Hence, I am sloving them in excel.

Part (a)

E(R) = P1r1+P2r2+P3r3

Hence, the expected return:

- HSCC =0.2 x 2% + 0.3 x 3% + 0.5 x 14% = 8.30%

- NINECENT = 0.2 x 16% + 0.3 x 10%+ 0.5 x 5% = 8.70%

Variance = P1 x (r1 - E(R))2 + P2 x (r2 - E(R))2+P3 x (r3 - E(R))2

Hence , variance for

- HSCC =0.2 x (2% - 8.30%)2+0.3 x (3% - 8.30%)2+0.5 x (14% - 8.30%)2 = 0.00326100

- NINECENT = 0.2 x (16% - 8.70%)2 + 0.3 x (10% - 8.70%)2 + 0.5 x (5% - 8.70%)2 = 0.00180100

Standard deviation = variance1/2 ; Hence std dev of

- HSCC = 0.003261001/2 = 5.71%

- NINECENT = 0.001801001/2 =4.24%

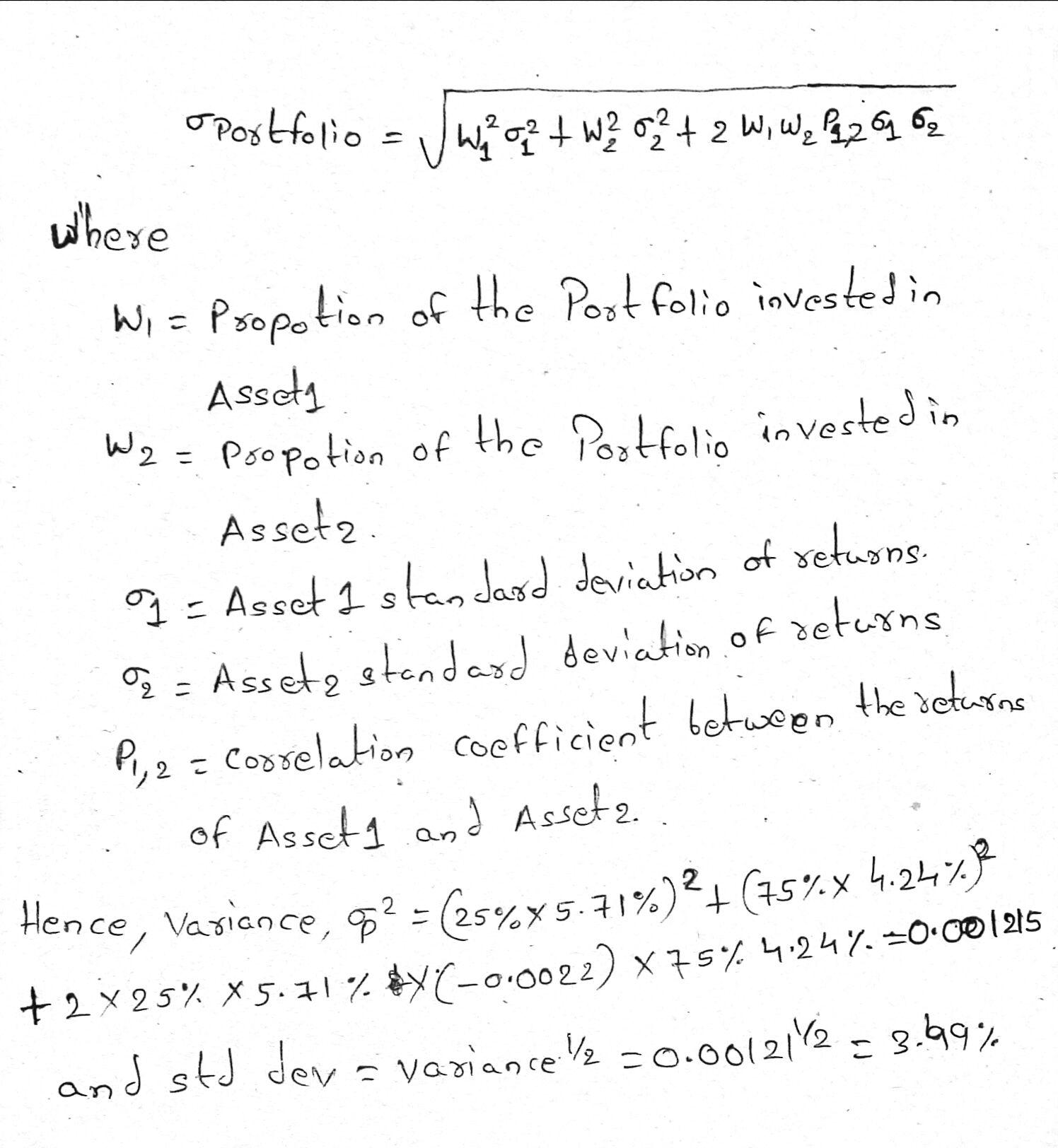

Part (B)

Let w be the proportion invested in HSCC .Hence , for a two stock ortfolio,

E(R) = w x E(R1) + (1 - w) x E(R2)

Hence, 8.6% = w x 8.30% + (1-w) x 8.70%

Hence, w = (8.70% - 8.60%) / (8.70% - 8.30%) = 0.25 = 25%

He should therefore invest 25% in HSCC,

For a two stock portfolio

and std dev = variance 1/2 = 0.001211/2 = 3.49%

Part (C)

Risk of the portfolio is lower than the weighted average risk because the individual stocks in the portfolio are negatively correlated. They have a naegative correlation, hence the portfolio gets the benfit of diversification and the portfolio risk is lower than the weighted average risk.

Part (d)

E(R) = Rf + beta x Rmp

Hence, using the CAMP model, the required rates of return of

- HSCC = 3% + 0.7 x 6% = 7.20%

- Ninecent = 3% + 1.3 x 6% =10.80%

Part (e)

HSCC:E(R) = 8.30% > E(R) using CAPM = 7.20%; Hence , this stock plots above the SML Hence, this security is undervalued / underoriced and hence sam should buy this.

Ninecent E(R) =8.70% < E(R) using CAMP = 10.80%. Hence, this stock plots below the SML Hence, this security is overvalued / overpriced and hence sam should not buy this.

Part(f)

While both beta and std dev measures risk, std deviation measures the total risk ( systematic as well as unsystemaic)While beta measures only the systematic risk. since they are measuring two different level of risks, the results of beta and standard deviation can be different even though both of them are measuring risk.

please see the attached file for the complete solution

{kind=link}

Archived Solution

You have full access to this solution. To save a copy with all formatting and attachments, use the button below.

For ready-to-submit work, please order a fresh solution below.