Why Choose Us?

0% AI Guarantee

Human-written only.

24/7 Support

Anytime, anywhere.

Plagiarism Free

100% Original.

Expert Tutors

Masters & PhDs.

100% Confidential

Your privacy matters.

On-Time Delivery

Never miss a deadline.

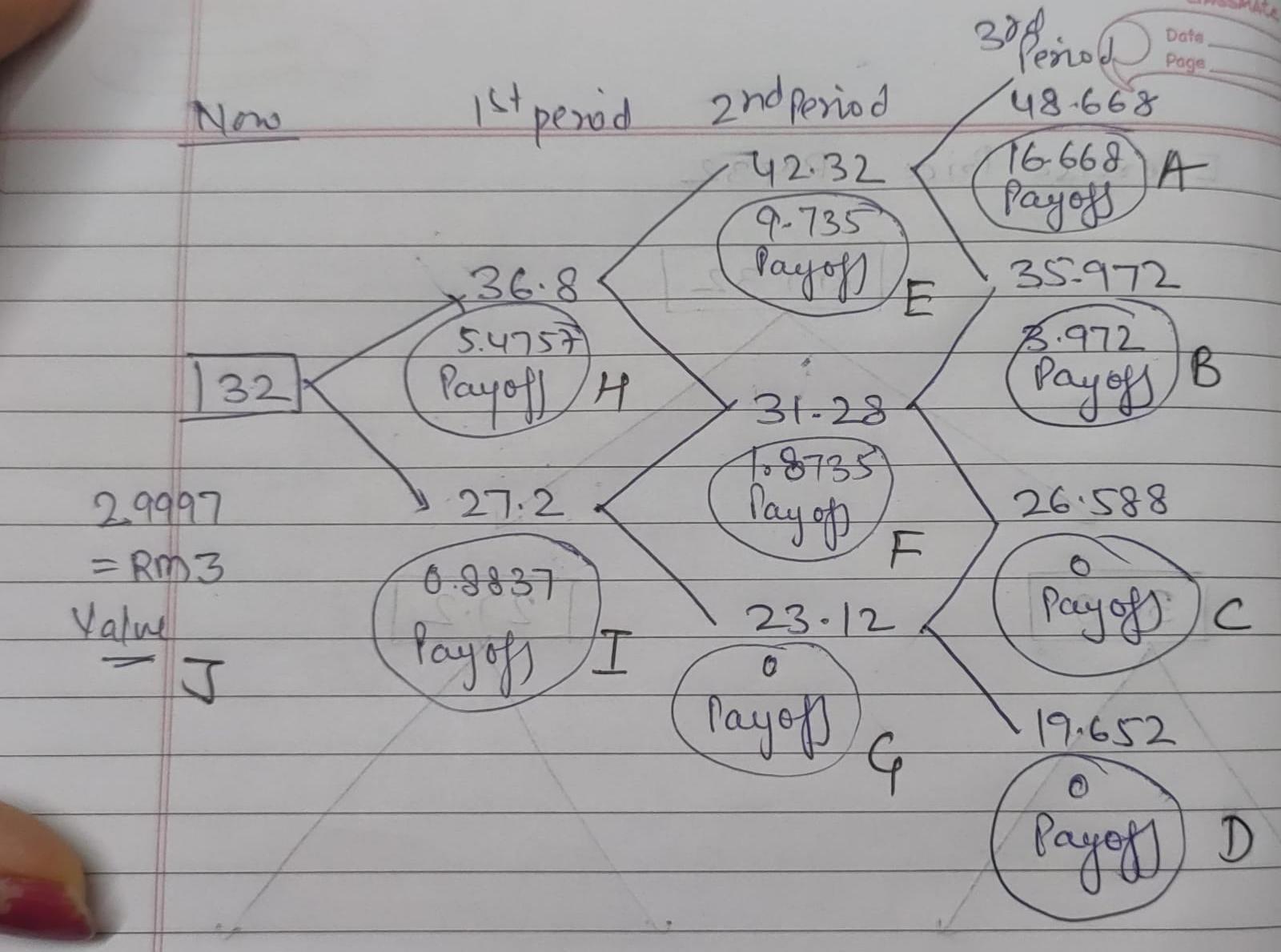

Construct a binominal option pricing model to calculate the value of a European style call option with the following information; Exercise price RM32 Volatility 15% Probability (up and down) 50% Risk free rate 6% per annum Price movement 3 times

Construct a binominal option pricing model to calculate the value of a European style call option with the following information; Exercise price RM32 Volatility 15% Probability (up and down) 50% Risk free rate 6% per annum Price movement 3 times

Expert Solution

For Calculation of stock price

Upward Movement 15% And downward movement 15%

For Calculation Of value of

A=48.668-32=16.668 ( Positive then Payoff, If negative then Pay-off is 0

B=35.972-32=3.972

C = 26.588-32=0

D = 190652-32=0

Now Probability Given is 50%=0.5 so, 1-P=1-0.5=0.5

Riskfree Rate if 6%

E = P*Upward payoff+(1-P)*Downward Payoff = 16.668*0.5+3.972*0.5 = 9.375

(1+Riskfree Rate) 1+0.06

Similarly

F = 3.972*0.5+0*0.5 = 1.8735

1.06

G = 0*0.5+0*0.5 = 0

1.06.

H = 9.735*0.5+1.8735*0.5 =5.4757

1.06

I = 1.8375*0.5+0*0.5 = 0.8837

1.06

J= Value of Option= 5.4757*0.5+0.8837*0.5 = 2.9997 =3

1.06

Value of Option is RM 3

please see the attached file for the complete solution

{kind=link}

Archived Solution

You have full access to this solution. To save a copy with all formatting and attachments, use the button below.

For ready-to-submit work, please order a fresh solution below.