Why Choose Us?

0% AI Guarantee

Human-written only.

24/7 Support

Anytime, anywhere.

Plagiarism Free

100% Original.

Expert Tutors

Masters & PhDs.

100% Confidential

Your privacy matters.

On-Time Delivery

Never miss a deadline.

In the long? run, all firms in a perfectly competitive industry? (assuming they have the same cost? curves) will be earning__ profits and will be producing at the ___ point of their?short-run ___ curve and the ___ point of their? long-run____ curve

In the long? run, all firms in a perfectly competitive industry? (assuming they have the same cost? curves) will be earning__ profits and will be producing at the ___ point of their?short-run ___ curve and the ___ point of their? long-run____ curve.

1/zero/positive/negative

2/maximum/minimum

3/average total cost marginal cost

4/maximum/minimum

5/average total cost marginal cost

Expert Solution

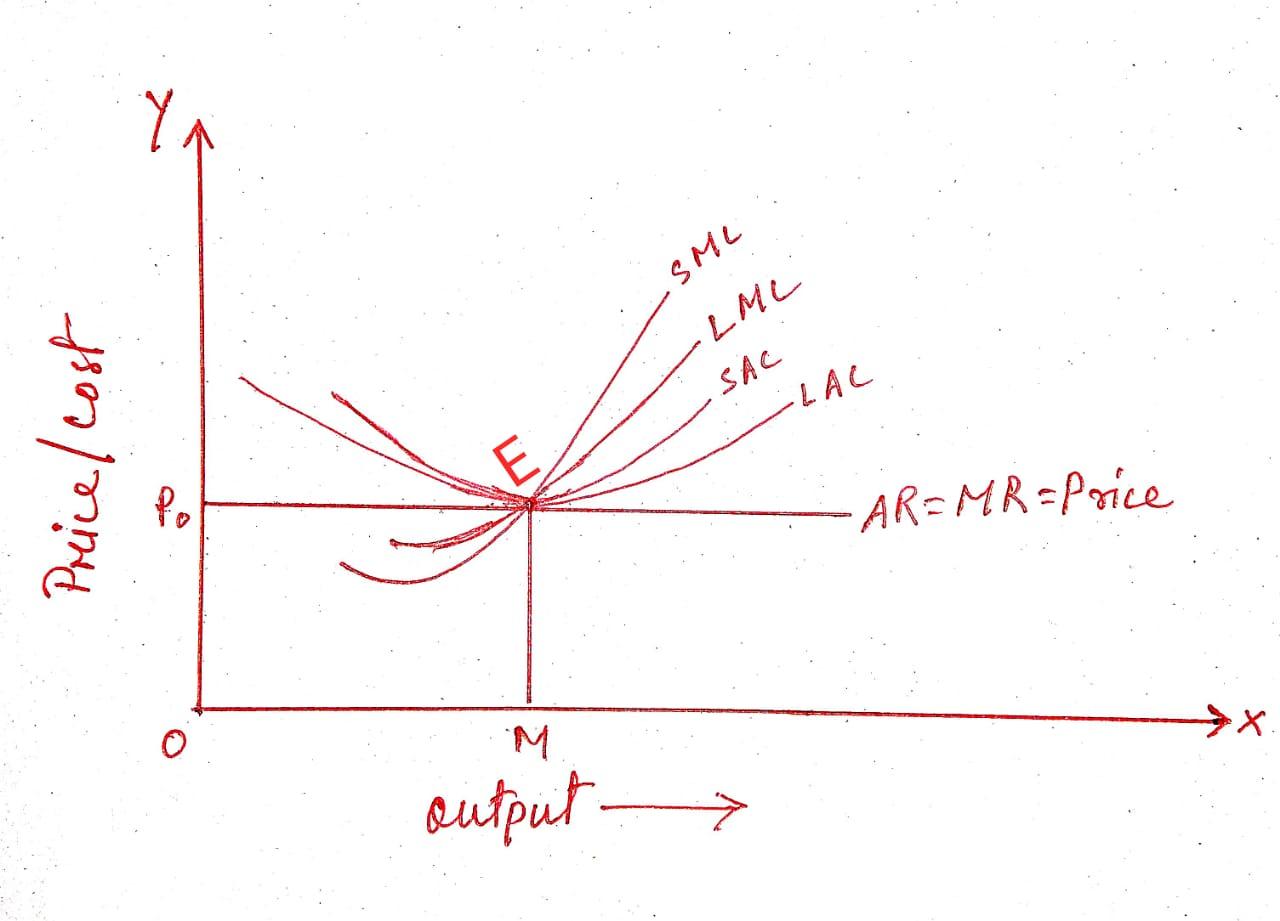

In the long? run, all firms in a perfectly competitive industry?(assuming they have the same cost? curves) will be earning zero (normal) profits and will be producing at the minimum point of their? short-run average total cost (SAC) curve and the minimum point of their? long-run average total cost (LAC) curve.

Explanation: In the long run, all the firms will be earning a normal profit where the Average cost of production is equal to the Average revenue (AR=Price). In the following figure we can see that at point E, the firm reaches its equilibirum where MR=AR=Price=SAC=LAC=SMC=LMC. Thus, at this point the Price is P0 and the quantity the firm producing is OM.

please see the attached file .

{kind=link}

Archived Solution

You have full access to this solution. To save a copy with all formatting and attachments, use the button below.

For ready-to-submit work, please order a fresh solution below.